Scovad

basset (NASDAQ:BSET), engages in furniture production and retail sales focused on the United States. The company is in an interesting spot at the moment, with Bassett facing weak demand and the disposal of Zenith Freight Lines in FY2022 contributing to this situation. a lower level of earnings. Financial recovery looks set to largely determine Bassett’s future stock performance.

The company’s stock return has historically been quite modest; The stock has gained 21% in the last decade. Bassett pays out a good amount of dividends, with a current yield of 4.33%.

Ten Year Stock Chart (Looking for Alpha)

Sale of Zenith Freight Lines – One Contributor to Declining Earnings

In March 2022, Bassett completed the sale of its logistics subsidiary Zenith Freight Lines to JB Hunt for approximately $87 million. Although the transaction significantly improved Bassett’s bottom lineThe sale had its drawbacks; Since the transaction was made, Bassett’s revenues and earnings have begun to decline, due in part to discontinued operations. The company’s current EBIT stands at $6.6 million, compared to the Fiscal Year 2022 figure of $29.8 million.

Third-party sales lost due to transaction represented In addition to using transportation services on its own, Bassett generated sales of approximately $16.8 million and operating income of $1.7 million in fiscal 2022. That same year, Zenith’s fees for the use of Bassett’s logistics services totaled approximately $9.1 million.

Bassett 2022 Annual Report

It is a bit too early to evaluate the long-term applications of the process; JB Hunt’s logistics network as a whole appears to have a wider reach and the improved network could provide some benefits as Bassett has signed a long-term deal with the company; Zenith assets should be better utilized under JB Hunt.

The macroeconomic situation, which is a more significant contributor to currently low earnings, is currently reducing Bassett’s sales level – Bassett’s management sees Although business is good due to holiday events, current demand for furniture is weak. Due to high freight costs during the pandemic, some of Bassett’s inventory is still marked as very high and makes a poor contribution to gross margins. As this impact fades, Bassett’s margins will return to a more historical level. The sale of Zenith assets has been attributed to lower earnings but does not appear to be the main driver.

Long-Term Financial Outlook

Looking at a longer-term horizon, Bassett’s growth looks quite modest, posting a revenue CAGR of 2.1% from FY 2002 to FY 2022. The furniture industry is fairly mature and stable, and Bassett doesn’t seem to have much differentiation in the industry to support market share growth; It seems likely that there will be a similar future in terms of revenues.

Calculation Made by the Author Using TIKR Data

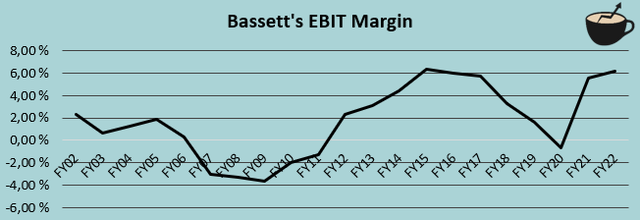

The more important question is how much of sales goes to the bottom line; Bassett’s long-term track record doesn’t seem to point to any clear numbers for the future. The company’s EBIT margin has fluctuated between -3.7% and 6.3%, with an average of 1.8% between FY 2002 and FY 2022:

Calculation Made by the Author Using TIKR Data

Margins Seem to Determine Bassett’s Course

In the case of investing, I believe investors should mostly keep a close eye on Bassett’s margin level. The company’s long-term margins have fluctuated significantly along with revenues, and the sale of Zenith assets creates further uncertainty about the future sustainable margin level.

I believe much of the current pressure on the company’s margins comes from lower gross margins than the company has achieved over the long term. From Fiscal Year 2013 through Fiscal Year 2022, Bassett’s average gross margin was 55.0%, compared to the current figure of 52.7%. If Bassett’s gross margin increases to the ten-year average, its EBIT margin will increase to 3.9% from its current level of 1.6%. I believe the current gross margin is lower than it should be in the medium-term future due to high freight costs associated with existing inventory and weak demand – I believe a recovery near the ten-year average is possible. a reasonable expectation.

Additionally, the lower sales level contributes negatively to EBIT margin beyond the lower gross margin due to fixed costs; A higher sales level should provide some operating leverage as the sales level recovers. Bassett was able to mitigate the impact of lower sales at the SG&A level through good cost control; Despite a good amount of inflation, Bassett’s SG&A decreased by approximately $6 million in the current fiscal year compared to the previous fiscal year’s numbers. The leverage higher sales would provide seems quite small, as the company has been able to shift costs but still provide some leverage to EBIT margin.

In summary, the currently low EBIT margin of 1.6% should not be considered a base case for a long-term margin. Once the macroeconomic situation improves, I believe Bassett has the ability to increase EBIT margin to a figure closer to 4% if gross margins improve. The margin estimate is still quite uncertain; As an investor, I recommend you to follow the margin trend closely.

Valuation

To contextualize Bassett’s valuation, I created a discounted cash flow model in my usual way. In the DCF model, I factor in sales recovery after FY 2023 with a growth forecast of 6% for FY 2024 and 3% for FY 2025. Following the recovery, I predict sustained revenue growth of 2%, in line with Bassett’s historical growth. In terms of margins, I forecast the recovery after a weak FY 2023 to eventually reach the 4.0% level achieved – I believe this figure represents a fair estimate of an achievable level over the long term.

Along with the estimates discussed, the DCF model with a cost of capital of 14.52% estimates Bassett’s fair value at $16.74; very close to the stock price at the time of this writing – I believe Bassett is priced with fair estimates of the company’s future financials.

DCF Model (Author’s Calculation)

The weighted average cost of capital employed is derived from a capital asset pricing model:

CAPM (Author’s Calculation)

Bassett’s balance sheet is very strong; The company’s debt does not include interest-bearing debt, except for very low interest payments from leases. As the company’s cash balance is quite large and earnings are at a lower level, I don’t see a scenario where Bassett will leverage financing, at least in the medium term; I estimate the debt/equity ratio will be 0%. future.

For the risk-free rate on the share cost side, I use the US 10-year bond yield of 4.45%. The equity risk premium of 5.91% is attributed to Professor Aswath Damodaran. last prediction It was made in July for the United States. Yahoo Finance estimates Bassett’s beta figure 1.62. Finally, I add a small liquidity premium of 0.5%, creating a cost of equity and a WACC of 14.52%.

take away

Bassett appears priced in for a partial revenue and margin recovery after FY2023. I believe the priced financial statements represent fair estimates of Bassett’s capabilities, as the company should be able to reduce gross margin and gain some operating leverage from a sales recovery. The previous divestiture of Zenith Freight Lines has clouded the financial picture a bit, but I think this transaction will be valuable in the long run as JB Hunt has the ability to manage the logistics department more efficiently. Right now the risk-reward balance seems balanced; I have a hold note for now.

#Bassett #Furniture #Eyeing #Financial #Recovery #NASDAQBSET